The Deal Failed. The Structure Held. Beijing Decides.

The Ceasefire That Wasn't. The Rally That Is

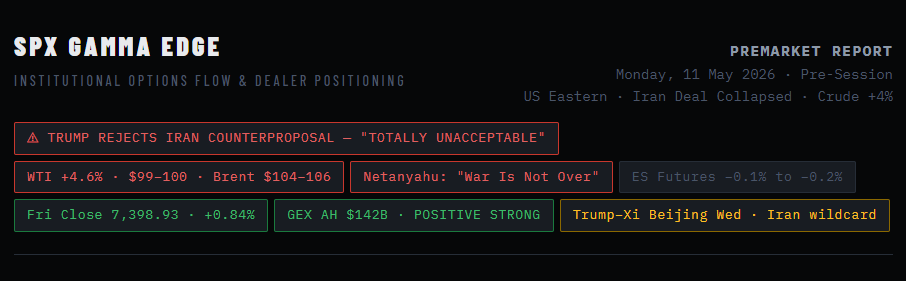

⚡ WEEKEND DEVELOPMENT — IRAN DEAL COLLAPSED SUNDAY

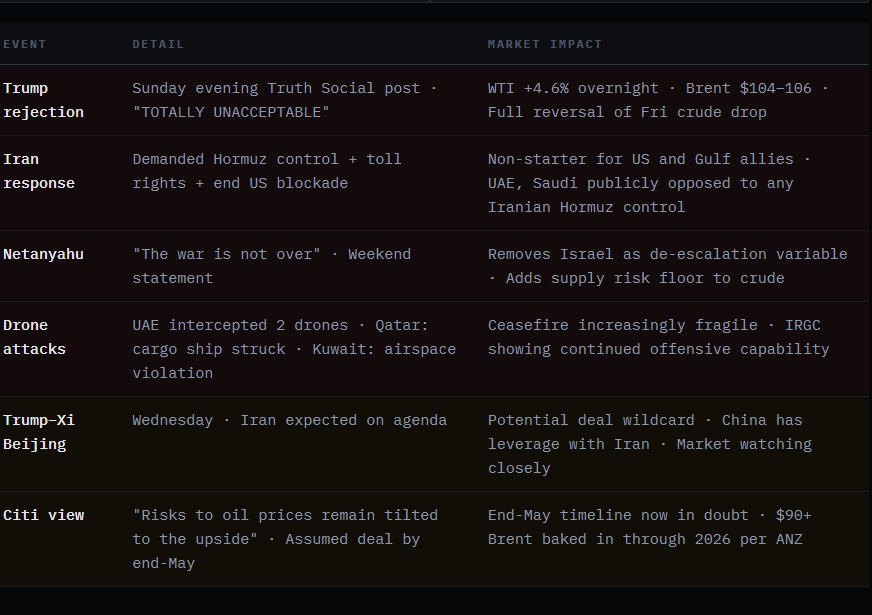

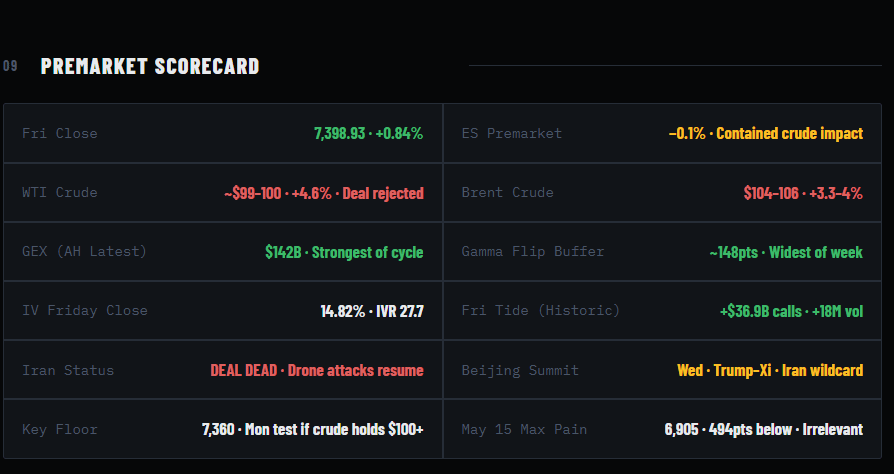

Trump rejected Iran’s counterproposal Sunday evening. Iran demanded management of the Strait of Hormuz and an end to the US blockade of Iranian exports. Trump called it “TOTALLY UNACCEPTABLE.” Tehran vowed to “never bow.” Netanyahu declared the war “not over.” Iran launched fresh drone attacks on UAE, Qatar, and Kuwait over the weekend. WTI surging +4.6% to $99–100. Brent at $104–106. Last week’s 6% crude decline — built entirely on deal optimism — is reversing.

THE DEAL COLLAPSED.

CRUDE RECLAIMS $100.

FRIDAY’S BULL CASE IS UNDER PRESSURE.

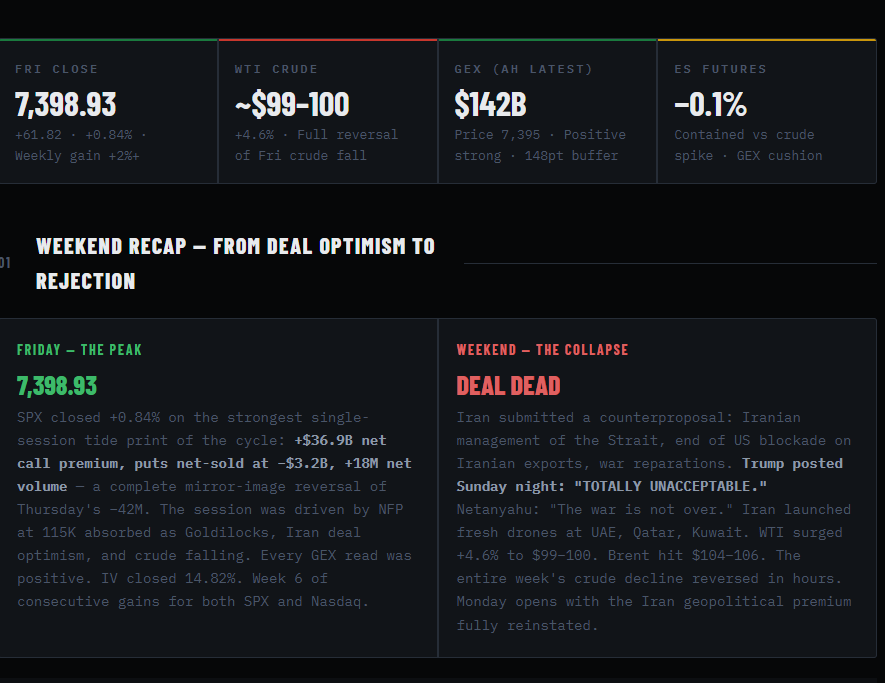

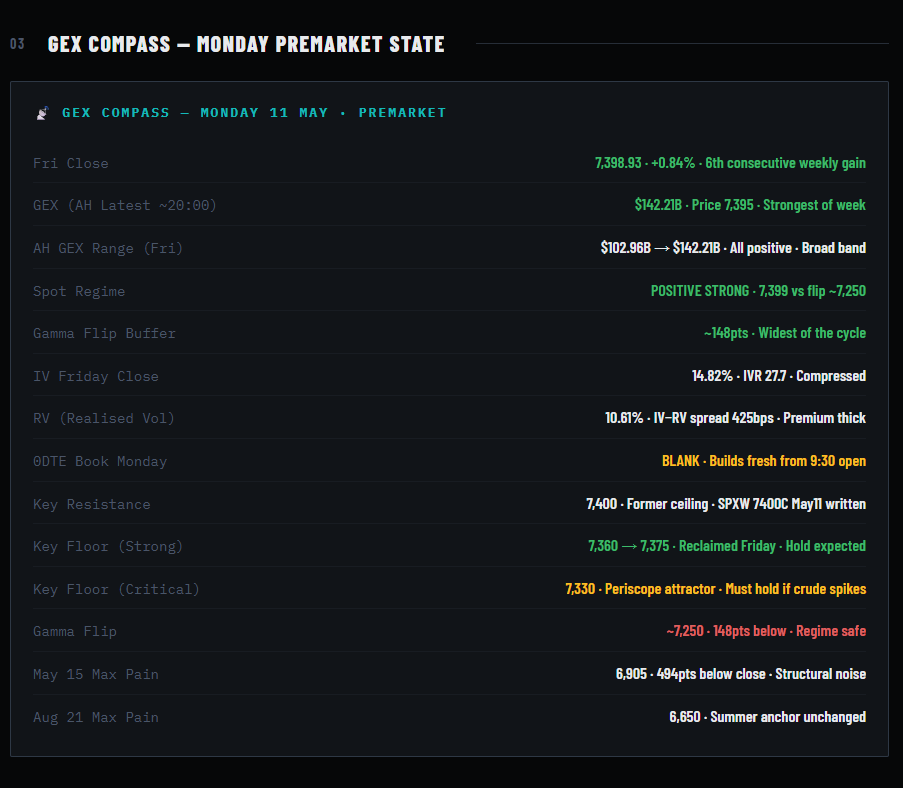

Friday closed at 7,398.93 on a week of extraordinary strength — the S&P 500 and Nasdaq logged their sixth consecutive winning week for the first time since 2024, riding NFP relief, Iran deal optimism, and the most bullish market tide in the cycle’s history (+$36.9 billion in net call premium, +18 million net volume). Then Sunday arrived. Trump rejected Iran’s counterproposal as “TOTALLY UNACCEPTABLE.” Tehran vowed to never surrender. Netanyahu declared the war unfinished. Drone attacks resumed across the Gulf. WTI is up 4.6% and approaching $100 again, unwinding essentially all of last week’s crude decline in a single overnight session. ES futures are only modestly lower, but that may not tell the full story. The GEX book is strong at ~$142B and the positive regime buffer is now 148 points — the widest of the cycle. The question Monday asks is whether a strong structural floor can hold against a renewed geopolitical premium in crude.

02: Friday Session Recap — Historic Tide Sets Up The Week

Friday Tide — Most Extreme Bull Session of the Entire Cycle

Friday’s market tide delivered a reading that made Thursday’s historic bearish print look like a rough draft. Cumulative: +$36.9B net calls, puts net-sold at −$3.2B, +17.998 million net volume. Every single bar from 9:30 AM through 4:10 PM was call-dominant. Puts were net-sold for the entire session — meaning institutions were not just buying calls, they were also selling put protection. Peak call flow: $628.3M at the 4:00 PM close bar. The 10:20 AM bar hit $459K net vol alone. This is the structural confirmation that Thursday’s −42M session was pre-NFP de-risking by the same institutions who then re-entered aggressively on Friday’s print. The two-day symmetry — extreme bear Wednesday to Thursday, then historic bull Friday — is textbook institutional position reset followed by reloaded longs.

GEX Friday Close — Regime Rebuilt to Strongest of the Week

Friday’s GEX opened at 7,370 with $92.2B and rebuilt steadily through the session. AH latest: $142.21B at price 7,395 — the highest GEX reading since the current rally began. Price range was tight: 7,365–7,400, locked in by dealer long-gamma mechanics. IV closed 14.82%, IVR 27.7 — compressed despite a session of large-scale call buying, confirming that the premium was being sold into rather than bid up. The gamma flip is estimated ~7,250, leaving a 148-point buffer — the widest of the entire week. This is a structurally strong GEX setup for Monday, providing significant mechanical support even against a moderate crude shock.

04: Flow Register — Friday AH Prints Write Monday’s Thesis

MU CALL · SAME-DAY + JAN27

$3.29M+

ASK + BID MIXED690C May8 $2.13M ASK + $1.16M ASK + $567K BID · Jan27 740C $209K ASK + 1050C $333K ASK · IV 85–124% · Vol 388+211+105

Micron 690C same-day bought in three tranches — $3.86M total into the final bell. MU at ~$662 → 690C is 4.2% OTM on expiry day, implying a massive final-hour move expected. The ascending/descending fills across multiple prints are consistent with a block being built by different desks simultaneously. The Jan27 740C and 1050C add structural layers: this is not a same-day lottery — it is a full stack from near-term to 8 months out. The ARM smartphone warning from earlier in the week has been completely overridden: institutions are loading DRAM exposure across the entire term structure.

IREN PUT · NOV 2026

$3.22M

BIDStrike 60 · Exp Nov 20 2026 · IV 102.1% · Vol 1,893 contracts · RepeatedHits · ~6-month tenor

$3.22M in Iris Energy puts — the largest single AH print of Friday’s session. IREN is an AI data center infrastructure and crypto mining company. At IV 102% and a 6-month tenor, this is not a routine hedge — it is an institutional bear position on a stock that has been one of the biggest AI infrastructure beneficiaries of the cycle. Two readings: either IREN-specific (operational risk, debt, overcapacity) or a proxy bet on energy cost inflation reversing AI data center economics if Hormuz stays closed and power costs remain elevated. The timing — placed at the exact moment Iran deal collapsed — suggests the second interpretation. If crude stays at $100+, power-intensive AI infrastructure names face margin compression.

TSLA PUT · DEC 2027

$2.85M

BIDStrike 400 · Exp Dec 17 2027 · IV 44.3% · Vol 369 contracts · RepeatedHits · 19-month tenor

$2.85M in TSLA 400P expiring December 2027 — the longest-dated bear position in the entire AH dataset. TSLA at ~$445 → 400P is 10% OTM with 19 months to expiry. This is a structural tail hedge against TSLA over a nearly two-year horizon. Compare to Friday morning’s aggressive TSLA call buying (425C May15, 450C Jun05, 440C Jul17 totalling $1.99M). The AH put purchase may be the same desk running a long-call / long-put book: bullish near-term via calls, hedged long-term via puts. Alternatively: a fund is expressing concern about TSLA’s EV competitive position, robotaxi execution risk, or Musk’s political exposure over a multi-quarter horizon.

INTC CALL · MAY 15

$1.81M

BID ASCStrike 131 · Exp May 15 · IV 105.6% · Vol 3,794 contracts · RepeatedHitsAscendingFill

$1.81M in Intel 131C May15 at IV 105.6% — a pure binary event bet. Intel at ~$125 → 131C requires +4.8% in 7 days. Ascending fill confirms institutional urgency: the buyer was chasing the price up rather than waiting. Intel has been reporting better-than-expected numbers in its foundry turnaround, and the ascending fill pattern suggests information or conviction that a catalyst arrives before May 15. Intel’s AI chip positioning and the CHIPS Act remain structural tailwinds. This is the largest single-name near-term call commitment in the flow register.

IWM PUT · JUN 18

$2.00M+

BID REPEATED270P Jun18 $688K + 269P Jun18 $664K + $651K desc · Three prints · IV 23.9–24.2% · Vol 1,981–2,019

$2.00M in IWM June puts across three tranches — the most concentrated small-cap hedge of the week. Three nearly identical prints at sequential strikes (269/270) all bought on the bid at similar IV, suggesting a single institutional position being scaled in. Small caps are more sensitive to rate expectations and domestic growth than large caps — a hot NFP reducing rate cut odds, combined with $100 crude pushing inflation higher, creates a genuine headwind for IWM that doesn’t apply equally to SPX. These Jun18 puts are not panic; they are a measured 5-week hedge against the scenario where tight monetary policy + energy inflation hits Main Street harder than Wall Street.

05: Iran Situation — Where The Negotiations Stand

The Core Impasse — Hormuz Sovereignty Is The Unbridgeable Gap

Iran’s counterproposal demanded Iranian management of the Strait of Hormuz — effectively sovereignty over the world’s most important energy chokepoint. The US, UAE, Saudi Arabia, and all Gulf allies have stated publicly this is completely unacceptable. This is not a negotiating position — it is a structural incompatibility. The US proposal sought: a 20-year halt to uranium enrichment, removal of enriched uranium stockpiles, dismantling of key nuclear facilities, and Iranian withdrawal from the Strait. Iran offered: transfer of some enriched uranium to a third country (but not dismantlement), Iranian control of Hormuz tolls, and US cessation of the blockade. The two positions are not close. The ceasefire itself is now fragile — Iran continued drone strikes on Gulf neighbours over the weekend, which the US has characterised as below the threshold for restarting major combat operations. But each drone incident raises that threshold risk.

Trump–Xi Beijing Wednesday — The Wildcard Variable

Trump is scheduled to arrive in Beijing on Wednesday. Iran is expected to be on the agenda alongside trade. China has unique leverage with Iran — as Iran’s largest oil customer and a diplomatic partner, Beijing has both economic and political tools to push Tehran toward a deal. If Xi signals to Trump that China will pressure Iran on Hormuz in exchange for trade concessions, a deal framework becomes more plausible. Market participants will be watching the Beijing meeting closely. Any joint US-China statement on Iran would be a major surprise catalyst for crude to fall and equities to rally. Conversely, if Beijing takes Iran’s side or signals neutrality, the impasse hardens. The Wednesday Beijing variable is the most important unknown on the Monday-to-Friday horizon.

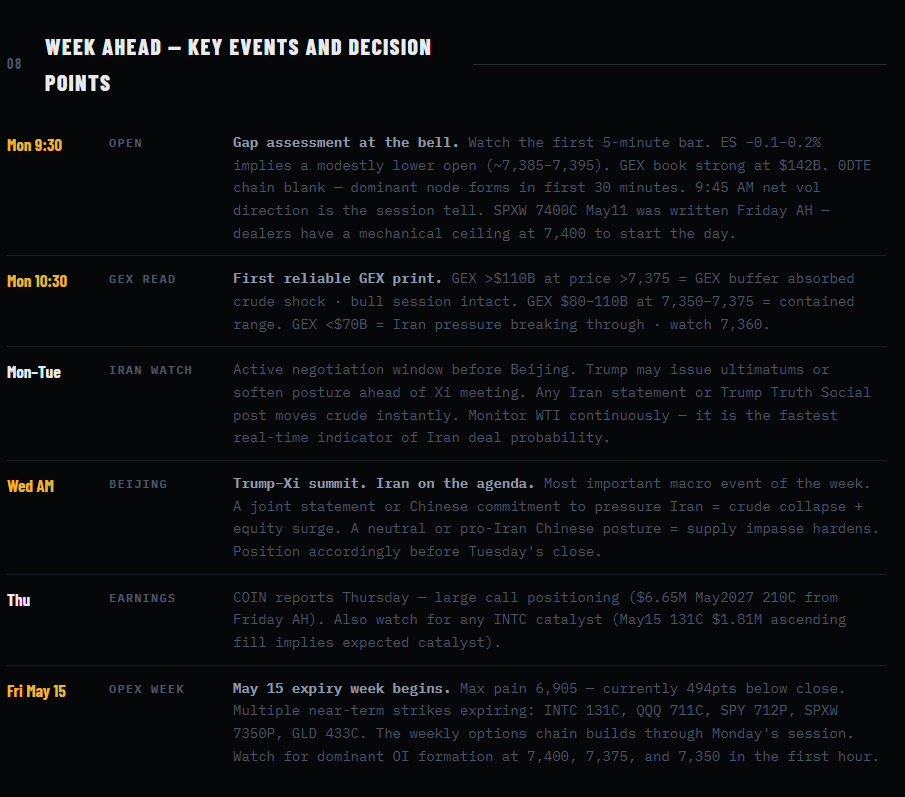

07: Trading Insights — Six Reads for Monday

01

The $142B GEX Is The Most Important Number Overnight

Despite crude surging 4.6%, ES is only −0.1–0.2%. The reason is the GEX book. $142B at 7,395 is the strongest mechanical support reading of the entire week — dealers are deeply long gamma and mechanically inclined to buy any dip. The 148-point gamma flip buffer means SPX would need to fall to 7,250 before the regime turns negative. A 4.6% crude move historically corresponds to approximately a 40–60 point SPX drag in isolation. The GEX structure is large enough to absorb that. Watch whether the 9:30 AM open prints below 7,360 on sustained volume — that is the level where GEX support begins to strain.

02

The SLV Put Is The Most Insightful Print in the Flow Register

Someone bought $649K in SLV June 72.5 puts on Friday AH — at the exact same time all week’s long SLV calls were being accumulated as a Hormuz inflation hedge. This is a hedge-on-the-hedge: protecting the silver long position against Iran deal completion. The fact that it appeared on Friday (when Iran deal optimism was near its peak) now reads as prescient — the deal collapsed within hours. The USO 125C call bought simultaneously for $215K is the other tell: that position is now in the money with crude at $99. Friday’s AH flow register contained both the bull and bear Iran catalysts — and the bear side activated over the weekend.

03

Beijing Wednesday Is The New Binary

The Iran MOU negotiation has shifted from a bilateral US-Iran dynamic to a trilateral involving China. Trump-Xi in Beijing on Wednesday is now the most important macro event of the week. If China signals willingness to pressure Iran on Hormuz reopening, crude falls 5–8% and equities gap higher. If Beijing takes a neutral or pro-Iran posture, the supply impasse hardens and crude stays elevated. Position sizing should reflect this: Monday and Tuesday are pre-Beijing uncertainty; Wednesday morning is the binary. Running large directional risk before Wednesday’s Beijing talks is a low-probability-of-being-right decision. Consider scaling rather than full positioning.

04

Friday’s Historic Tide Cannot Be Dismissed as a Setup Trap

+$36.9B net call premium in a single session is not retail noise. That is institutional money expressing maximum near-term conviction in higher prices. The Friday session was driven by desks that de-risked Thursday and re-entered Friday at lower prices — and they came back with significantly more size than they left with. The Thursday −42M / Friday +18M tide symmetry over two days is one of the most dramatic institutional position pivots in recorded market data. These buyers did not sell over the weekend; they are waking up to Monday with large call positions. The Iran deal collapse creates pressure, but not necessarily an unwind — these positions still have time value and the GEX structure is strong.

05

Crude $100 Is Not the Same As Crude $110

WTI at $99–100 is the level that was tolerated by equities for most of April and early May. The market knows how to price $100 crude — it already has been doing it. The inflationary concern from $100 oil is largely priced into both CPI expectations and equity multiples. What changes the calculus is a move toward $110–120 — that is the level where gasoline prices cross political thresholds, the Fed’s hands get tied explicitly, and consumer spending pressure becomes material. Watch the $104 Brent level: if it holds or fades, Monday is a contained dip. If it breaks above $106–108 on escalation headlines, the second-order impacts begin to matter.

06

The IREN Put Is An Energy Cost Warning for AI Infrastructure

The $3.22M IREN put at IV 102% for 6 months is the most structurally interesting print in Friday’s AH dataset. IREN is a high-power AI data center and mining operator — its margins are directly exposed to electricity costs, which correlate with natural gas and crude oil prices. If Hormuz stays closed and LNG supply stays constrained through summer, power costs in data-intensive geographies (Texas, Australia, Nordic) remain elevated. The bet against IREN is a bet that crude-linked energy costs compress AI infrastructure margins over the next two quarters. This is not a stock-specific trade — it is a sector-level call on energy cost normalization failing to materialize. Broader AI infra names should be watched for sympathy.

“Friday built the strongest GEX fortress of the week. Sunday tore down the diplomatic scaffolding around it. The question for Monday is not whether the market can absorb this — it already has, mostly — but whether it can hold long enough for Beijing to matter.”

Verdict

The Deal Failed. The Structure Held. Beijing Decides The Week.

Sunday’s Iran rejection should have cratered equity futures. It didn’t. ES is down a modest 0.1–0.2% despite WTI surging 4.6% and Brent hitting $104–106 — a crude move that in any other context would register as a significant macro shock. The reason for the contained futures response is written in Friday’s GEX data: $142.21B at 7,395, the strongest dealer long-gamma position of the entire rally cycle, backed by 148 points of positive-regime buffer above the gamma flip. The same institutional desks that generated +$36.9B in net call premium on Friday are waking up Monday with large long positions and a structurally thick mechanical floor underneath. They are not panicking. And when institutional desks with $36.9B of call premium don’t panic on Iran deal collapse, the market’s self-stabilizing properties are telling you something about where conviction sits.

The AH flow from Friday now reads like a two-sided picture in hindsight. The MU call stack ($3.29M), INTC binary ($1.81M), NVDA cluster ($860K+), AMD ascending fill ($603K), and SPY Jun 2027 long call ($549K) are the bull positions — all built on the thesis that the AI capex cycle and semiconductor demand transcend geopolitical noise. The IREN $3.22M put, TSLA Dec 2027 $2.85M put, IWM $2.00M put cluster, SPXW Jul 7390P ($527K), and SPX Jun 7150P ($328K) are the hedge layer — all expressing concern about a sustained crude premium compressing margins, elevating rates, and weighing on economically-sensitive sectors over a 4–12 week horizon. Both sides are intellectually coherent. The next week will determine which framework was right, and the determining variable is not a chart level — it is a diplomatic meeting in Beijing on Wednesday.

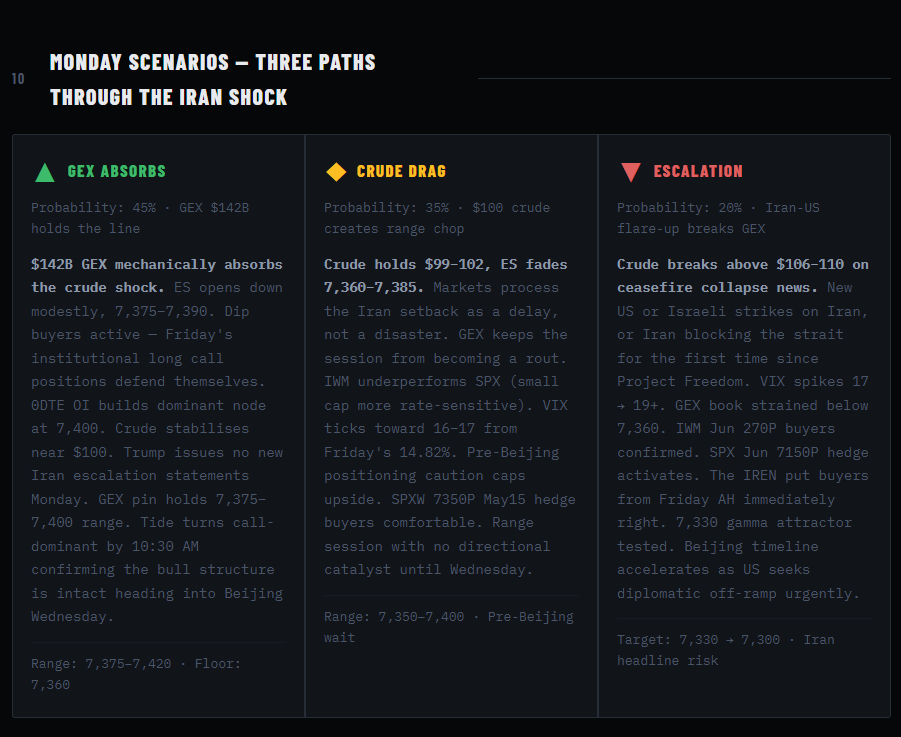

The week’s structure is clear: Monday and Tuesday are pre-Beijing uncertainty, during which the GEX floor provides mechanical support and the 7,360–7,400 range is the most likely trading band absent a fresh Iran escalation headline. Wednesday’s Trump-Xi summit is the binary. China has both economic leverage over Iran (as its largest oil buyer) and diplomatic standing (as the world’s second-largest power) that the US lacks unilaterally. If Beijing commits to pressuring Tehran on Hormuz reopening, the crude shock reverses and the bull case accelerates through 7,420 toward new highs. If Beijing remains neutral or sides with Iran, the supply impasse hardens, Citi’s end-of-May timeline slips, and the market must price Brent above $100 as the new structural floor. The Friday AH USO call buyer already knows this. So does the IREN put buyer. Watch Brent. Watch Beijing. They are the same trade.

▲ GEX Absorbs: 7,375–7,420 · Structure holds◆ Crude Drag: 7,350–7,400 · Pre-Beijing wait▼ Escalation: 7,330–7,300 · Crude >$106⚡ Watch: 9:45 tide · Brent tick · Wed Beijing

Disclaimer

SPX Gamma Edge publishes options flow and dealer positioning analysis for informational and educational purposes only. Nothing herein constitutes financial advice, investment recommendations, or solicitation to buy or sell any security or derivative. Options trading involves substantial risk of loss. Past positioning signals do not guarantee future performance. Always conduct your own due diligence and consult a qualified financial professional before making any trading decision.

© 2026 SPX Gamma Edge. All rights reserved.