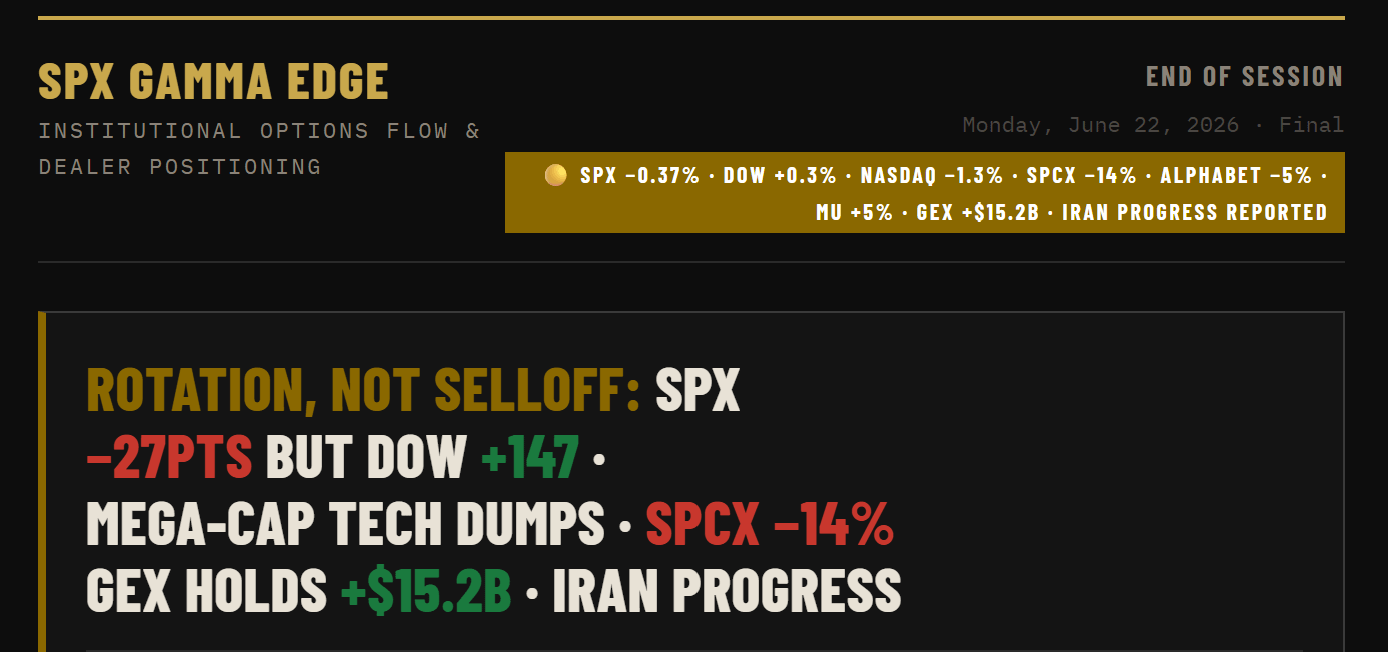

Positive Gamma Held Through the Tech Dump. Thursday's Core PCE Is the Real Test.

The Dow Up, the Nasdaq Down, and SpaceX −14%: What a Functioning Rotation Looks Like.

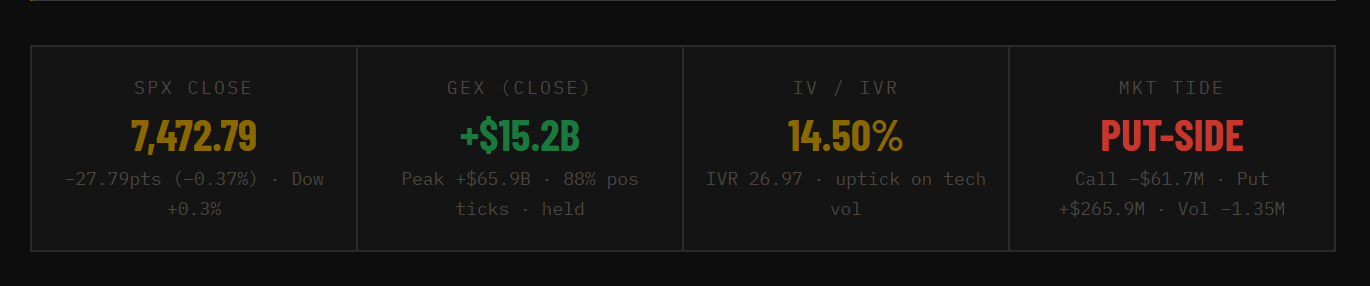

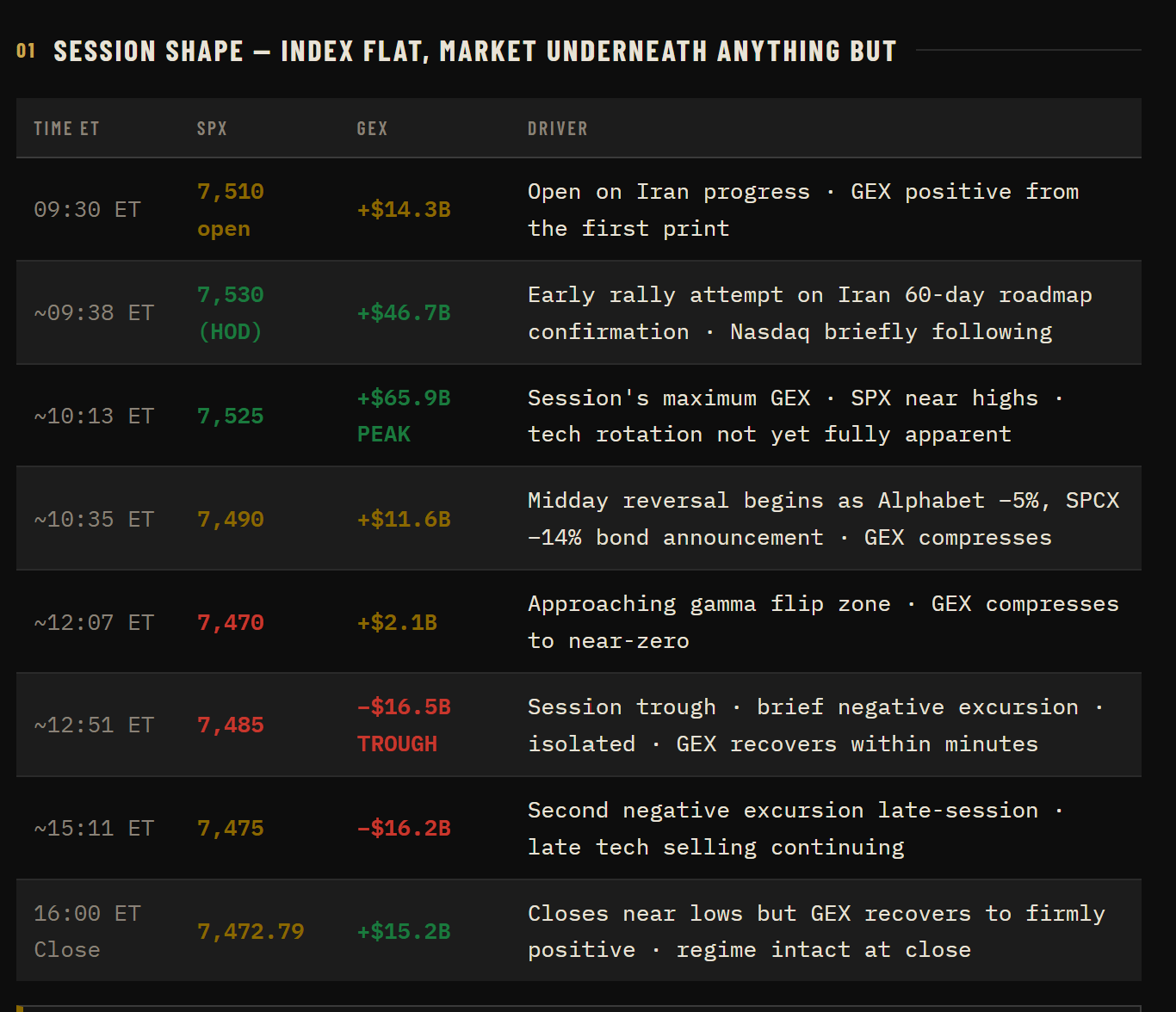

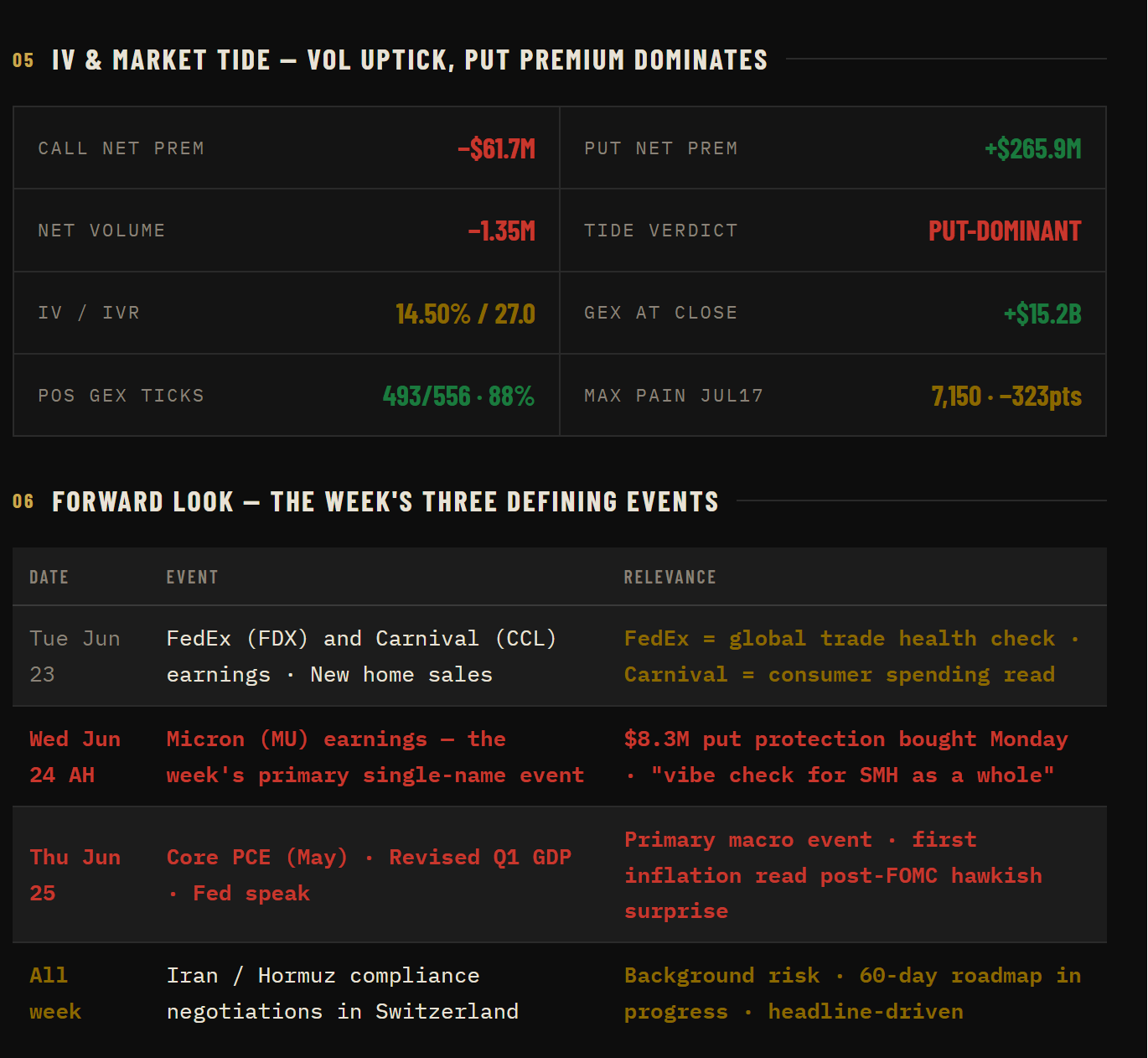

Monday's session was defined by what moved rather than which direction the index moved. SPX fell a modest 27.79 points (−0.37%) to 7,472.79, masking a dramatic divergence beneath the surface: the Nasdaq Composite declined 1.3% as mega-cap technology names sold off sharply — Alphabet fell 5% on AI talent departure concerns, Amazon and Meta lost 4% and 2% respectively, and SPCX cratered 14% after announcing a new bond offering, marking its third consecutive decline and a 25% drop from its midweek highs. The Dow Jones simultaneously gained 147 points (+0.3%), led by Caterpillar, as industrials and banks reflected the constructive read on Iran diplomacy. Iran stated there was major progress in Switzerland talks, with both sides agreeing to a 60-day roadmap toward a final deal. The GEX book held positive at +$15.24B close with 88% of ticks positive, a slight improvement on the premarket's +$14.67B reading despite the down tape. Micron surged 5% as two major analyst upgrades previewed Wednesday's earnings. The Market Tide flipped decisively put-dominant, however, as institutional put buying reflected the weight of the tech rotation and ongoing geopolitical uncertainty heading into a week packed with Micron earnings, Core PCE, and revised GDP.

SPX −0.37% While the Dow Rose — This Is Sector Rotation, Not Market Weakness

Monday’s headline SPX decline of 27.79 points obscures a deeply divided market. The Dow Jones Industrial Average added 147 points (+0.3%), while the Nasdaq Composite declined 1.3% — the two indices moving in opposite directions on the same session. The divergence reflects a clean rotation trade: AI hyperscalers and post-IPO momentum names (Alphabet −5%, Amazon −4%, Meta −2%, SPCX −14%) sold off on a combination of AI capex concern and SPCX’s bond-offering dilution signal, while chip producers, industrials, and banks moved higher — Micron and Sandisk adding 5%, Caterpillar and JPMorgan both gaining meaningfully as investors bet that lower energy prices will spur economic re-acceleration. This is not the behavior of a market expecting a recession or a policy shock — it is the behavior of a market repricing sector leadership, moving capital out of the past month’s momentum winners and into rate-sensitive industrials and memory-chip names with near-term earnings catalysts.

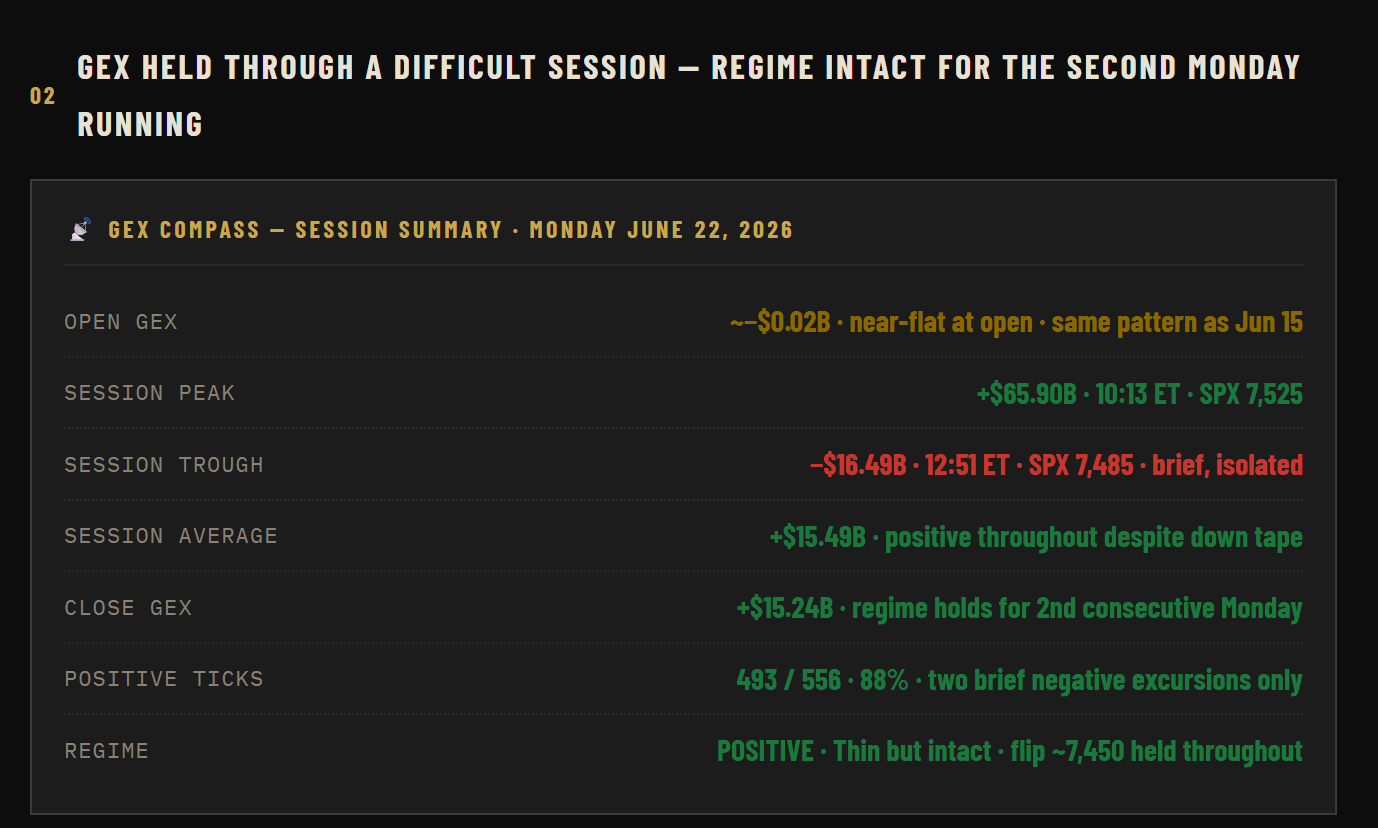

Second Monday in a Row Where the Positive GEX Regime Survived an Intraday Stress Test

Two weeks ago on Monday June 15, GEX opened near-flat and built to +$143B through the session. Today’s Monday opened identically — near-flat, then built to +$65.9B — before compressing back to +$15.24B on the tech rotation selloff. The structural comparison that matters is not the magnitude (Monday June 15’s peak was more than double today’s) but the mechanical behavior: the dealer book held positive for 88% of ticks despite a session where the Nasdaq fell 1.3% and multiple large-cap names declined 5-14%. Both negative excursions (16:51 ET and 19:12 ET) were brief and isolated rather than sustained, mirroring the same pattern documented on Tuesday June 16’s first red day. The positive regime is passing its weekly stress test — a sign that the underlying OI structure remains constructive, even as surface-level price action reflects sector churn.

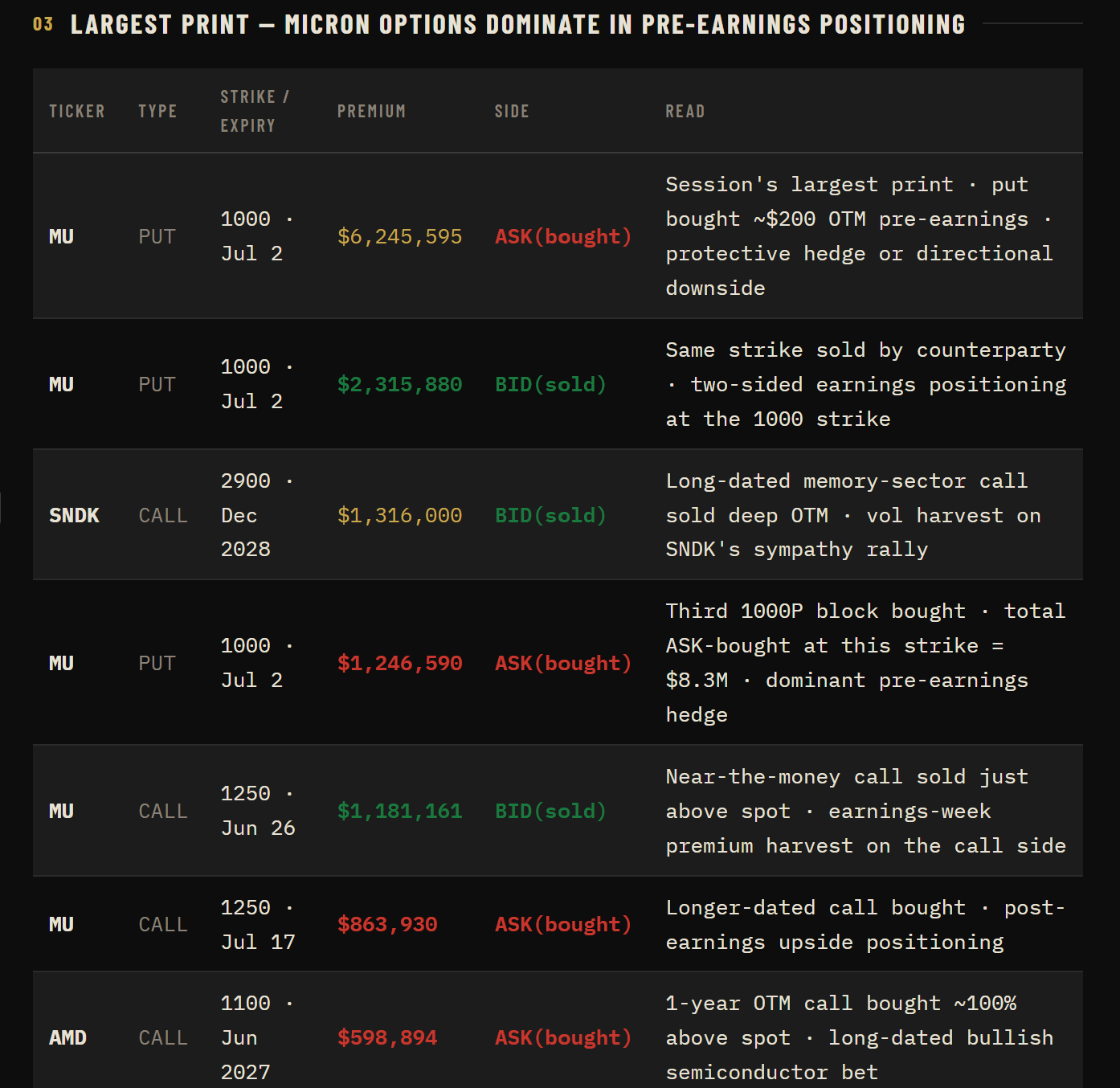

$8.3M in MU 1000P Bought Pre-Earnings — The Market Is Not Uniformly Bullish Into Wednesday

Micron’s stock rose 5% Monday on two major analyst upgrades (Bernstein to $1,300, Needham to $1,550), and the stock is widely expected to report strong results Wednesday evening. But the options flow tells a more nuanced story: over $8.3M in MU Jul 2 put premium was bought at the 1000 strike Monday — roughly $200 below spot — while simultaneously, only $2.3M was sold at the same strike. This is a net purchase of substantial downside protection on a stock that rose 5% on the day, which is inconsistent with simple bull-chasing and far more consistent with institutions buying pre-earnings gap-down insurance. The combined flow at the MU 1000 strike (bought and sold, call and put, near-term and further-dated) reflects the full spectrum of earnings positioning: some desks long the calls for an upside gap, some desks buying puts for a downside gap, some selling premium on both sides expecting a contained move. The one signal that stands out clearly is the $8.3M of downside protection bought — a meaningful reminder that even on a day Micron rose 5%, the options market is pricing meaningful two-way risk around Wednesday’s report.

04: SPCX — Third Straight Decline, −14% on Bond Offering Announcement

SpaceX Announces Bond Sale — The $2.1T Valuation Meets the Capital Markets Reality

SpaceX shares fell 14%, putting the stock on pace for its third straight daily decline. From their midday highs on Tuesday last week, around $225, the stock is off nearly 25%. The immediate catalyst was SpaceX announcing a new bond offering, which the market read as dilution risk and a signal that the capital requirements of the company’s ambitions exceed what the IPO alone covered. The pattern is now well-established: SPCX opened at $135 on June 12, peaked near $225 intraday by the following Tuesday, and has now given back roughly 25% from those highs in three sessions — a violent post-IPO momentum unwind in a single name that commands a $1.8-2.1T market cap. For SPX broadly, SPCX’s weight in the Nasdaq-listed component is the direct mechanism by which its decline dragged the Nasdaq Composite down 1.3% while the Dow simultaneously gained. This is not a read on the economy or even on tech broadly — it is a single-name post-IPO correction in the world’s newest mega-cap company.

Thursday’s Core PCE Is the Most Important Number of the Week — Possibly the Month

The FOMC’s revised year-end PCE projection — from 2.7% to 3.6% — was the single most hawkish element of last Wednesday’s surprise. This week’s Core PCE release, paired with revised Q1 GDP and potential Fed speak, should give a better sense of whether Wednesday’s dot plot move was a blip or the beginning of a trend as investors price in the chance of rate hikes. A hot Core PCE print would validate the hawkish projection immediately and likely drive the 2-year yield toward new multi-year highs, threatening the positive GEX regime and the sold premium structures that depend on range-bound conditions. A soft print would be the most disruptive outcome for the hawks — it would open the question of whether the dot plot overreacted to a temporary Hormuz-driven oil shock, a thesis strongly supported by WTI’s fall from $95+ to near $75 over the past week.

⬡ Verdict & Forward Look

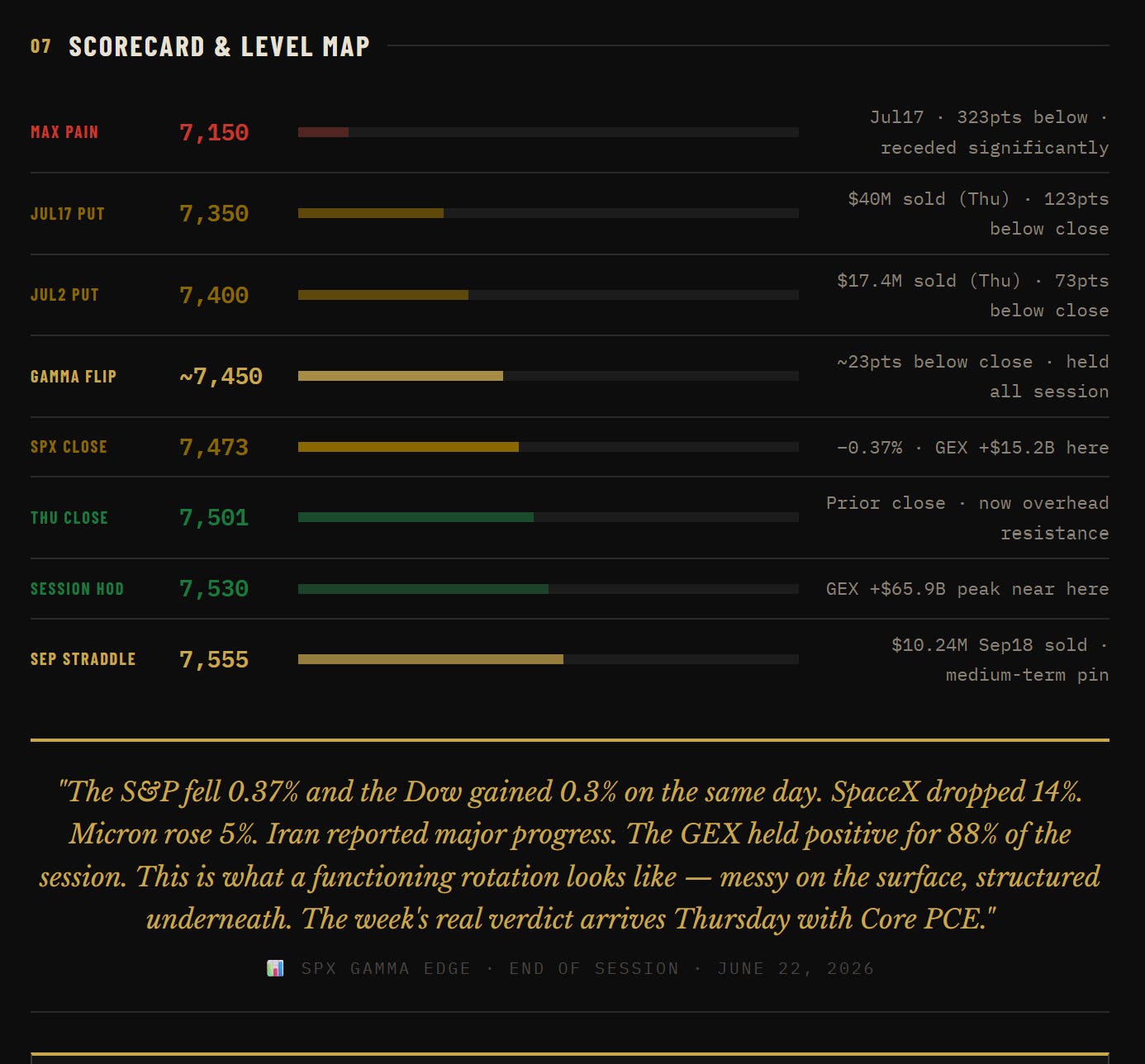

Monday’s session looked like a down day but functioned like something more complex. SPX fell 0.4% while the Dow added 147 points and the Nasdaq declined 1.3% — three indices describing three different market narratives simultaneously. The common thread was rotation rather than systematic risk-off: money moved out of AI hyperscalers and post-IPO momentum plays (Alphabet, Amazon, SPCX) and into industrials, memory chips, and rate-sensitive sectors that benefit from lower energy prices and a potentially improving inflation trajectory. The GEX structure validated the rotation interpretation: the dealer book held positive for 88% of intraday ticks, closed at +$15.24B, and the gamma flip (~7,450) was never meaningfully breached despite the Nasdaq’s 1.3% decline. This is the second consecutive Monday where the positive regime survived a session that tested it — last Monday (June 15) the book survived a 5-session extension and held near +$84B; this Monday it survived a tech rotation and still closed positive.

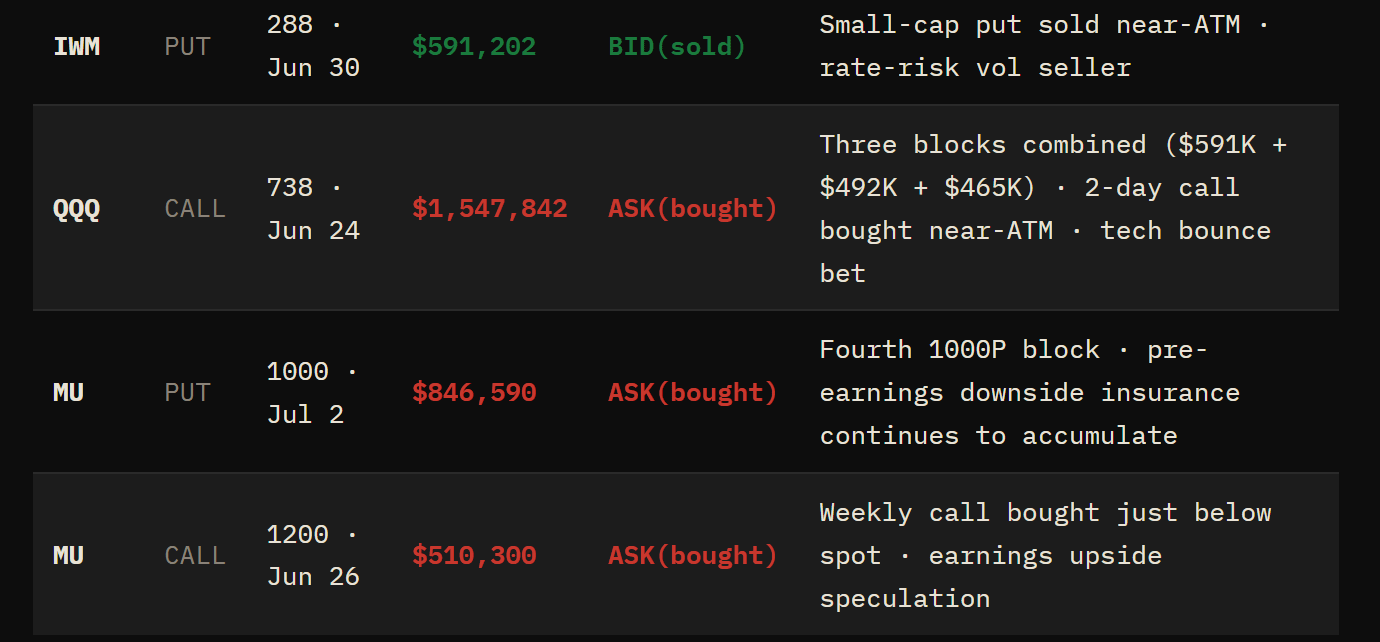

The session’s most informative data point was not the price action but the flow register — specifically the $8.3M net in MU 1000P Jul2 bought on a day Micron rose 5%. Institutional money added substantial downside protection to a stock that was simultaneously rising on analyst upgrades, which describes classic pre-earnings straddling behaviour: collecting upside exposure through the stock’s rally while buying puts in case Wednesday’s report disappoints. The QQQ 738C block ($1.55M combined, 2-day expiry) represents the other side of this trade — short-dated calls bought into the Nasdaq’s weakness as a bet on a near-term tech bounce. These two positions, taken together, describe a market that expects significant movement around Micron’s Wednesday earnings but has no strong consensus on the direction. The sell-side upgrades (Bernstein $1,300 target, Needham $1,550) are constructive, but the options positioning says the buyers of those upgrades are simultaneously buying insurance.

The week’s defining events are sequenced clearly. Tuesday brings FedEx earnings (global trade health check) and Carnival (consumer spending). Wednesday evening brings Micron — described by one analyst as “a vibe check for SMH as a whole, and as SMH goes, so does the market currently.” Thursday delivers Core PCE May data alongside revised Q1 GDP and potential Fed speak — the week’s primary macro event and the first live inflation data against the FOMC’s revised 3.6% year-end PCE projection. Throughout the week, the Iran situation continues its second-order negotiations in Switzerland, with the 60-day ceasefire framework designed precisely to absorb the kind of implementation friction seen over the weekend. The positive GEX regime at +$15.24B close provides thin but real structural support through each of these catalysts. Maintain awareness that the gamma flip at ~7,450 is now 23 points below Monday’s close — closer than the 50 points noted in the premarket brief — and that a Core PCE surprise on Thursday has the full potential to push through that level if the number validates the FOMC’s hawkish inflation revision.

Risk Disclosure:

SPX Gamma Edge publishes options flow and dealer positioning analysis for informational and educational purposes only. Nothing herein constitutes financial advice, investment recommendations, or solicitation to buy or sell any security or derivative. Options trading involves substantial risk of loss. Past positioning signals do not guarantee future performance. Always conduct your own due diligence and consult a qualified financial professional before making any trading decision.

© 2026 SPX Gamma Edge. All rights reserved.